프로바이오틱스 음료 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Probiotic Drinks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드

:

1750346

리서치사

:

Global Market Insights Inc.

발행일

:

2025년 05월

페이지 정보

:

영문 220 Pages

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

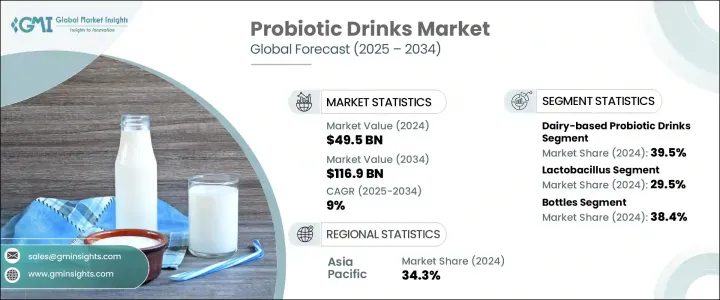

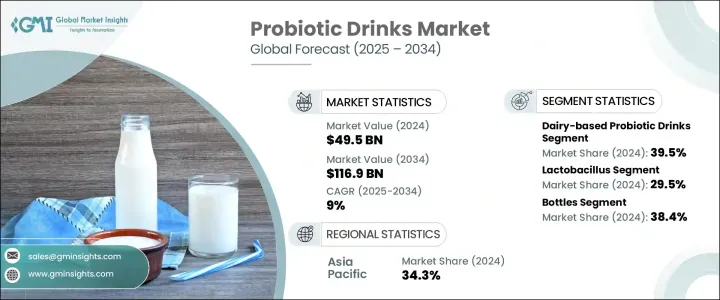

세계의 프로바이오틱스 음료 시장은 2024년에는 495억 달러로 평가되었고, 장 건강, 면역력 및 종합적인 웰빙에 대한 소비자의 관심이 증가함에 따라 CAGR 9%로 성장할 전망이며, 2034년에는 1,169억 달러에 이를 것으로 추정됩니다.

당초에는 요구르트와 보충제에 한정되어 있던 프로바이오틱스 제품은 그 후, 기능성 음료, 유아용 조제 분유, 나아가 동물사료에까지 발전하고 있습니다. 시장의 성장을 지지하고 있는 것은 프로바이오틱스의 건강 효과를 확인하는 과학적 조사와, 소비자 의식의 고조입니다.

프로바이오틱스 음료 수요는 선진국 시장과 신흥국 시장 모두에서 높아지고 있으며, 특히 북미, 유럽, 아시아태평양에서 높은 성장세를 보이고 있습니다. 아시아태평양 시장은, 인구의 많고, 가처분 소득의 증가, 식생활의 기호의 변화에 의해, 가장 높은 성장률이 전망되고 있습니다. 게다가 인구의 고령화와 대사성 질환이나 위장 질환의 증가가, 프로바이오틱스 기반의 제품에 대한 수요를 촉진하고 있습니다. 조사에 따르면 식음료, 특히 유제품에 프로바이오틱스를 도입함으로써 소비자의 수용성과 제품의 안정성이 크게 향상되어 시장이 확대되고 있습니다.

| 시장 범위 |

| 시작 연도 |

2024년 |

| 예측 연도 |

2025-2034년 |

| 시작 금액 |

495억 달러 |

| 예측 금액 |

1,169억 달러 |

| CAGR |

9% |

유제품 베이스의 프로바이오틱스 음료 부문은 2024년에 39.5%의 점유율을 차지했습니다. 이러한 음료는 높은 영양가 때문에 여전히 인기가 높고 요구르트 음료 및 케피어가 특정 지역에서 우위를 유지하고 있습니다. 그러나 시장은 식물 기반 프로바이오틱스 음료로의 전환을 목격하고 있습니다. 이 변화는 비건, 락토오스 프리, 알레르겐 프리의 대체품에 대한 수요 증가가 주요 요인이 되고 있습니다. 콩, 아몬드, 코코넛, 귀리 등을 원료로 하는 음료는 그 맛과 건강상의 이점 때문에 인기를 끌고 있습니다.

프로바이오틱스 음료 시장은 프로바이오틱스 균주별로 분류되며, 2024년에는 유산균이 29.5%의 점유율을 차지하여 선도했습니다. L. 람노서스나 L. 아시도필루스 등의 유산균주는 소화기계의 건강을 촉진하고 면역력을 높이는 것으로 잘 알려져 있습니다. 비피담균이나 롱검균 같은 다른 균주는 특히 노인이나 어린이의 건강한 장내 균형 유지에 도움이 됩니다. 프로바이오틱스의 이점에 대한 소비자들의 인식이 높아짐에 따라 이들 균주가 시장 확대의 원동력이 될 것으로 예상됩니다.

아시아태평양 프로바이오틱스 음료 2024년 시장 점유율은 34.3%였습니다. 이 지역은 급속한 성장을 이루고 있어 일본과 같은 나라들은 과학적 뒷받침이 있는 프로바이오틱스 제품에 주력하고 있는 반면, 중국이나 인도는 요구르트 및 콤부차와 같은 건강 지향의 음료를 점점 받아들이고 있습니다. 북미에서도 웰니스 동향이 높아지면서 마시는 요구르트나 콤부차 등의 기능성 음료의 수요가 높아지고 있습니다.

In the Global 프로바이오틱스 음료 Market, companies like Yakult Honsha Co.Ltd., Groupe Danone SA, The Fonterra Co-op Group Ltd., Kerry Group PLC, Groupe Lactalis 등의 기업은 시장에서의 존재감을 높이기 위해서 중요한 전략을 채용하고 있습니다. 이러한 전략에는, 폭넓은 기능성 음료나 식물성 음료를 포함한 제품 포트폴리오의 확대, 제품의 품질을 높이기 위한 선진 생산 기술의 활용, 환경을 배려한 포장 및 조달 관행에 의한 지속 가능성의 동향에 대한 대응 등이 포함됩니다. 게다가 이러한 기업은, 변화하는 소비자의 기호에 맞는 혁신적인 제품을 만들어내기 위한 연구 개발에 투자하고 있어, 제품의 안정성의 향상과 건강 효과의 강화에 주력하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 제조업자

- 리셀러

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망 및 향후 검토 사항

- 공급자의 상황

- 이익률 분석

- 주요 뉴스 및 대처

- 규제 상황

- 북미

- 유럽

- 유럽식품안전기관(EFSA) 가이드라인

- EU의 건강 강조 표시 규제

- 아시아태평양

- 특보규제(일본)

- CFDA 규제(중국)

- FSSAI 규제(인도)

- 세계 기타 지역

- 영향요인

- 성장 촉진요인

- 개인화된 건강 및 웰빙 요구

- 지속가능성 및 윤리적 조달

- 식물 유래 및 유제품 이외의 대체품으로의 이행

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용

- 프로바이오틱스 생존 능력 유지에서의 과제

- 시장 기회

- 신흥 시장으로 확대

- 제품 배합에서의 혁신

- 전자상거래 및 소비자 직접 판매 채널의 성장

- 식물 유래의 대체품에 대한 수요 증가

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 제조 공정과 기술

- 제조 공정 개요

- 원재료 조달 및 준비

- 프로바이오틱스 배양액의 조제

- 발효 및 가공

- 배합 및 블렌드

- 포장 및 보관 전략

- 생산 비용 분석

- 원재료비

- 처리 비용

- 인건비

- 포장 비용

- 제조 간접비

- 비용 최적화 전략

- 제조 시설 분석

- 공급망의 과제 및 해결책

- 원재료 조달

- 공급망 전체의 품질 관리

- 콜드체인 관리

- 재고 관리

- 품질 보증 및 관리

- 미생물 검사

- 안정성 및 보존 기간의 시험

- 관능 평가

- 소비자 행동 및 시장 동향의 분석

- 소비자의 기호와 구매 패턴

- 소비자의 인구 통계 분석

- 소비자의 의식 및 교육

- 새로운 소비자 동향

- 디지털 변혁이 소비자 참여에 미치는 영향

- 소비자 피드백 분석 및 그 영향

- 가격 동향 분석

- 가격에 영향을 미치는 요인

- 제품 부문 전체의 가격 전략

- 프리미엄 시장 및 매스 시장의 포지셔닝

- 가치 기반 가격 설정 접근법

- 지역별 가격 변동 및 그 요인

- 가격과 가치의 관계 분석

- 시장에 영향을 미치는 경제지표

- 프로바이오틱스 음료의 현재 기술 동향

- 신흥기술 및 그 잠재적인 영향

- 제품 혁신 동향

- 기능성 성분의 조합

- 상온 보존 가능한 프로바이오틱스 솔루션

- 포장 혁신

- 지속가능한 포장 재료

- 액티브하고 지능적인 포장

- 생산과 유통에서 디지털 기술

- IoT 및 스마트 제조

- 추적성을 위한 블록체인

- 연구개발 활동 및 혁신허브

- 지역별 기술 도입 동향

- 아시아태평양이 기능성 음료 기술 도입으로 리드

- 생산 기술의 지속가능성을 중시하는 유럽

- 미래의 기술 로드맵(2025-2033년)

- 개인화된 프로바이오틱스 솔루션 개발

- 품질 관리 시스템의 자동화 및 AI

- 마케팅 전략 및 브랜드 분석

- 현재 마케팅 상황

- 디지털 마케팅 전략

- 종래의 마케팅 기법

- 건강 커뮤니케이션 전략

- 주요 기업의 브랜드 분석

- 마케팅 도구로서의 패키지

- 미래 마케팅 동향과 전략

- 시장 기회 및 전략적 제안

- 미개척 시장 기회

- 시장 진출 기업에 대한 전략적 제안

- 제품 개발 전략

- 시장 진입 및 확대 전략

- 경쟁 우위 구축 전략

- 미래 성장 경로

- 리스크 평가 및 경감 전략

- 시장 위험

- 운영 위험

- 규제 및 규정 준수 위험

- 평판 위험

- 환경 및 지속가능성의 위험

- 리스크 경감 전략 및 프레임워크

- 미래 전망 및 시장 발전

- 장기 시장 예측(2025-2035년)

- 미래 시장 시나리오

- 낙관적 시나리오

- 현실적인 시나리오

- 비관적인 시나리오

- 신흥 제품 카테고리 및 혁신

- 소비자 기호 및 행동의 진화

- 기술의 진화 및 그 영향

- 지속가능성과 순환형 경제의 발전

- 미래경쟁 구도

- 장기적인 성공을 위한 전략적 필수 사항

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 유제품 베이스 프로바이오틱스 음료

- 프로바이오틱스 요구르트 음료

- 케피아

- 프로바이오틱스 우유 음료

- 기타

- 식물 유래의 프로바이오틱스 음료

- 두유 음료

- 아몬드 기반 음료

- 코코넛 기반 음료

- 기타

- 과일 및 채소 베이스의 프로바이오틱스 음료

- 프로바이오틱스 과일 주스

- 프로바이오틱스 야채 주스

- 과일 및 채소 믹스 음료

- 수성 프로바이오틱스 음료

- 발효 프로바이오틱스 음료

- 프로바이오틱스 기능성 음료

- 프로바이오틱스 에너지 음료

- 프로바이오틱스 스포츠 음료

- 프로바이오틱스 웰니스 샷

제6장 시장 추계 및 예측 : 프로바이오틱스 균주별(2021-2034년)

- 주요 동향

- 유산균

- 비피더스균

- 연쇄상 구균

- 바실러스

- 사카로미세스

- 다균주 제형

제7장 시장 추계 및 예측 : 포장 형태별(2021-2034년)

제8장 시장 추계 및 예측 : 타겟 소비자 그룹별(2021-2034년)

- 주요 동향

- 일반 성인 인구

- 아이 및 청소년

- 고령자 인구

- 운동 선수 및 피트니스 애호가

- 건강 지향의 소비자

제9장 시장 추계 및 예측 : 소비 씬별(2021-2034년)

- 주요 동향

- 1일 소비량

- 식사 대체품

- 외출처에서의 소비

- 운동 후 회복

제10장 시장 추계 및 예측 : 가격대별(2021-2034년)

- 주요 동향

- 이코노미 및 매스마켓

- 미드레인지

- 프리미엄 및 고급

제11장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 슈퍼마켓 및 하이퍼마켓

- 편의점

- 전문건강식품점

- 병원 약국 및 소매 약국

- 온라인 소매

- 푸드서비스 부문

제12장 시장 추계 및 예측 : 판매 채널별(2021-2034년)

제13장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제14장 기업 프로파일

- Yakult Honsha Co.,Ltd.

- Danone SA

- Nestle SA

- PepsiCo, Inc.

- Coca-Cola Company

- Lifeway Foods, Inc.

- Harmless Harvest

- KeVita(PepsiCo)

- GoodBelly(NextFoods)

- Chobani, LLC

- Groupe Lactalis

- Bio-K Plus International Inc.

- Fonterra Co-operative Group Juicery

AJY

영문 목차

The Global Probiotic Drinks Market was valued at USD 49.5 billion in 2024 and is estimated to grow at a CAGR of 9% to reach USD 116.9 billion by 2034, driven by a surge in consumer interest in gut health, immunity, and overall wellness. Initially limited to yogurt and supplements, probiotic products have since evolved to include functional beverages, infant formulas, and even animal feed. The market's growth is supported by scientific research confirming the health benefits of probiotics, as well as increasing consumer awareness.

Demand for probiotic drinks is rising across both developed and emerging markets, with particularly high growth in North America, Europe, and the Asia-Pacific region. The Asia-Pacific market is expected to experience the highest growth rates due to its large population, increasing disposable income, and changing dietary preferences. Additionally, an aging population and a rise in metabolic and gastrointestinal disorders are driving the demand for probiotic-based products. Research has shown that incorporating probiotics into food and beverages, especially in dairy products, has significantly increased consumer acceptance and product stability, expanding the market.

| Market Scope |

|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $49.5 Billion |

| Forecast Value | $116.9 Billion |

| CAGR | 9% |

Dairy-based probiotic drinks segment held a 39.5% share in 2024. These drinks remain popular for their nutritional value, with yogurt drinks and kefir continuing to dominate in certain regions. However, the market is witnessing a shift toward plant-based probiotic drinks. This change is largely driven by growing demand for vegan, lactose-free, and allergen-free alternatives. Drinks made from ingredients like soy, almond, coconut, and oat are gaining popularity for their taste and health benefits.

The probiotic drinks market is categorized by probiotic strains, with Lactobacillus taking the lead, representing a 29.5% share in 2024. Lactobacillus strains such as L. rhamnosus and L. acidophilus are well-known for promoting digestive health and boosting immunity. Other strains like B. bifidum and B. longum help maintain a healthy gut balance, especially in the elderly and children. As consumer awareness of the benefits of probiotics grows, these strains are expected to drive market expansion.

Asia-Pacific Probiotic Drinks Market held a 34.3% share in 2024. The region is experiencing rapid growth, with countries like Japan focusing on science-backed probiotic products, while China and India are increasingly embracing health-conscious beverages like yogurt and kombucha. North America is also seeing a rise in wellness trends, with a growing demand for functional beverages such as drinkable yogurts and kombucha.

In the Global Probiotic Drinks Market, companies like Yakult Honsha Co. Ltd., Groupe Danone SA, The Fonterra Co-op Group Ltd., Kerry Group PLC, and Groupe Lactalis are adopting key strategies to strengthen their market presence. These strategies include expanding product portfolios to include a wider range of functional and plant-based drinks, leveraging advanced production technologies to enhance product quality, and aligning with sustainability trends through eco-friendly packaging and sourcing practices. Additionally, these companies are investing in research and development to create innovative products that meet changing consumer preferences, focusing on improving product stability and enhancing health benefits.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.1.6 Impact on trade

- 3.1.7 Trade volume disruptions

- 3.2 Retaliatory measures

- 3.3 Impact on the industry

- 3.3.1 Supply-side impact (raw materials)

- 3.3.1.1 Price volatility in key materials

- 3.3.1.2 Supply chain restructuring

- 3.3.1.3 Production cost implications

- 3.4 Demand-side impact (selling price)

- 3.4.1 Price transmission to end markets

- 3.4.2 Market share dynamics

- 3.4.3 Consumer response patterns

- 3.5 Key companies impacted

- 3.6 Strategic industry responses

- 3.6.1 Supply chain reconfiguration

- 3.6.2 Pricing and product strategies

- 3.6.3 Policy engagement

- 3.7 Outlook and future considerations

- 3.8 Supplier landscape

- 3.9 Profit margin analysis

- 3.10 Key news & initiatives

- 3.11 Regulatory landscape

- 3.12 North America

- 3.12.1 FDA regulations (United States)

- 3.12.2 Health Canada regulations

- 3.13 Europe

- 3.13.1 European Food Safety Authority (EFSA) Guidelines

- 3.13.2 EU health claims regulation

- 3.14 Asia Pacific

- 3.14.1 FOSHU regulations (Japan)

- 3.14.2 CFDA regulations (China)

- 3.14.3 FSSAI regulations (India)

- 3.15 Rest of the world

- 3.16 Impact forces

- 3.16.1 Growth drivers

- 3.16.1.1 Personalized health and wellness needs

- 3.16.1.2 Sustainability and ethical sourcing

- 3.16.1.3 Shift toward plant-based and non-dairy alternatives

- 3.16.2 Industry pitfalls & challenges

- 3.16.2.1 High production costs

- 3.16.2.2 Challenges in maintaining probiotic viability

- 3.16.3 Market Opportunities

- 3.16.3.1 Expansion in emerging markets

- 3.16.3.2 Innovation in product formulations

- 3.16.3.3 Growth of E-commerce and direct-to-consumer channels

- 3.16.3.4 Rising demand for plant-based alternatives

- 3.17 Growth potential analysis

- 3.18 Porter's analysis

- 3.19 PESTEL analysis

- 3.20 Manufacturing process and technology

- 3.20.1 Manufacturing process overview

- 3.20.1.1 Raw material procurement and preparation

- 3.20.1.2 Probiotic culture preparation

- 3.20.1.3 Fermentation and processing

- 3.20.1.4 Formulation and blending

- 3.20.1.5 Packaging and storage strategies

- 3.20.2 Production cost analysis

- 3.20.2.1 Raw material costs

- 3.20.2.2 Processing costs

- 3.20.2.3 Labor costs

- 3.20.2.4 Packaging costs

- 3.20.2.5 Manufacturing overheads

- 3.20.2.6 Cost optimization strategies

- 3.20.3 Manufacturing facilities analysis

- 3.20.3.1 Facility expansion plans

- 3.20.4 Supply chain challenges and solutions

- 3.20.4.1 Raw material sourcing

- 3.20.4.2 Quality control throughout supply chain

- 3.20.4.3 Cold chain management

- 3.20.4.4 Inventory management

- 3.20.5 Quality assurance and control

- 3.20.5.1 Microbial testing

- 3.20.5.2 Stability and shelf-life testing

- 3.20.5.3 Sensory evaluation

- 3.21 Consumer behavior and market trends analysis

- 3.21.1 Consumer preferences and purchasing patterns

- 3.21.2 Demographic analysis of consumers

- 3.21.3 Consumer awareness and education

- 3.21.4 Emerging consumer trends

- 3.21.5 Impact of digital transformation on consumer engagement

- 3.21.6 Consumer feedback analysis and implications

- 3.22 Pricing trends analysis

- 3.22.1 Factors affecting pricing

- 3.22.1.1 Raw material costs

- 3.22.1.2 Production and processing costs

- 3.22.2 Pricing strategies across product segments

- 3.22.2.1 Premium vs. mass market positionings

- 3.22.2.2 Value-based pricing approaches

- 3.23 Regional price variations and factors

- 3.24 Price-value relationship analysis

- 3.25 Economic indicators impacting the market

- 3.26 Current technological trends in probiotic drinks

- 3.26.1 Emerging technologies and their potential impact

- 3.26.1.1 Microencapsulation technologies

- 3.26.1.2 Synbiotic formulations

- 3.26.2 Product innovation trends

- 3.26.2.1 Functional ingredient combinations

- 3.26.2.2 Shelf-stable probiotic solutions

- 3.26.3 Packaging innovations

- 3.26.3.1 Sustainable packaging materials

- 3.26.3.2 Active and intelligent packaging

- 3.26.4 Digital technologies in production and distribution

- 3.26.4.1 IoT and smart manufacturing

- 3.26.4.2 Blockchain for traceability

- 3.26.5 R&D activities and innovation hubs

- 3.26.6 Technology adoption trends across regions

- 3.26.6.1 Asia-pacific leading in functional drink tech adoption

- 3.26.6.2 Europe emphasizing sustainability in production tech

- 3.26.7 Future technology roadmap 2025-2033

- 3.26.7.1 Development of personalized probiotic solutions

- 3.26.7.2 Automation and ai in quality control systems

- 3.27 Marketing strategies and brand analysis

- 3.27.1 Current marketing landscape

- 3.27.2 Digital marketing strategies

- 3.27.3 Traditional marketing approaches

- 3.27.4 Health communication strategies

- 3.27.5 Brand analysis of key players

- 3.27.6 Packaging as a marketing tool

- 3.27.7 Future marketing trends and strategies

- 3.28 Market opportunities and strategic recommendations

- 3.28.1 Untapped market opportunities

- 3.28.2 Strategic recommendations for market participants

- 3.28.3 Product development strategies

- 3.28.4 Market entry and expansion strategies

- 3.28.5 Competitive advantage building strategies

- 3.28.6 Future growth pathways

- 3.29 Risk assessment and mitigation strategies

- 3.29.1 Market risks

- 3.29.1.1 Demand fluctuations

- 3.29.1.2 Competitive pressures

- 3.29.2 Operational risks

- 3.29.2.1 Supply chain disruptions

- 3.29.2.2 Production challenges

- 3.29.3 Regulatory and compliance risks

- 3.29.3.1 Changing food safety regulations

- 3.29.3.2 Labeling and claims regulations

- 3.29.4 Reputational risks

- 3.29.5 Environmental and sustainability risks

- 3.29.6 Risk mitigation strategies and frameworks

- 3.30 Future outlook and market evolution

- 3.30.1 Long-term market forecast 2025-2035

- 3.30.2 Future market scenarios

- 3.30.2.1 Optimistic scenario

- 3.30.2.2 Realistic scenario

- 3.30.2.3 Pessimistic scenario

- 3.30.3 Emerging product categories and innovations

- 3.30.4 Evolving consumer preferences and behaviors

- 3.30.5 Technological evolution and its impact

- 3.30.6 Sustainability and circular economy developments

- 3.30.7 Future competitive landscape

- 3.30.8 Strategic imperatives for long-term success

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Liters)

- 5.1 Key trends

- 5.2 Dairy-based probiotic drinks

- 5.2.1 Probiotic yogurt drinks

- 5.2.2 Kefir

- 5.2.3 Probiotic milk drinks

- 5.2.4 Others

- 5.3 Plant-based probiotic drinks

- 5.3.1 Soy-based drinks

- 5.3.2 Almond-based drinks

- 5.3.3 Coconut-based drinks

- 5.3.4 Others

- 5.4 Fruit and vegetable-based probiotic drinks

- 5.4.1 Probiotic fruit juices

- 5.4.2 Probiotic vegetable juices

- 5.4.3 Mixed fruit and vegetable drinks

- 5.5 Water-based probiotic drinks

- 5.5.1 Probiotic water

- 5.5.2 Probiotic sparkling beverages

- 5.6 Fermented probiotic beverages

- 5.6.1 Kombucha

- 5.6.2 Kvass

- 5.6.3 Others

- 5.7 Probiotic functional beverages

- 5.7.1 Probiotic energy drinks

- 5.7.2 Probiotic sports drinks

- 5.7.3 Probiotic wellness shots

Chapter 6 Market Estimates and Forecast, By Probiotic Strain, 2021 - 2034 (USD Billion) (Kilo Liters)

- 6.1 Key trends

- 6.2 Lactobacillus

- 6.3 Bifidobacterium

- 6.4 Streptococcus

- 6.5 Bacillus

- 6.6 Saccharomyces

- 6.7 Multi-strain formulations

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Billion) (Kilo Liters)

- 7.1 Key trends

- 7.2 Bottles

- 7.3 Cartons

- 7.4 Cans

- 7.5 Pouches

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Target Consumer Group, 2021 - 2034 (USD Billion) (Kilo Liters)

- 8.1 Key trends

- 8.2 General adult population

- 8.3 Children and Adolescents

- 8.4 Elderly population

- 8.5 Athletes and fitness enthusiasts

- 8.6 Health-conscious consumers

Chapter 9 Market Estimates and Forecast, By Consumption Occasion, 2021 - 2034 (USD Billion) (Kilo Liters)

- 9.1 Key trends

- 9.2 Daily consumption

- 9.3 Meal replacement

- 9.4 On-the-Go consumption

- 9.5 Post-exercise recovery

Chapter 10 Market Estimates and Forecast, By Price Segment, 2021 - 2034 (USD Billion) (Kilo Liters)

- 10.1 Key trends

- 10.2 Economy / mass market

- 10.3 Mid-range

- 10.4 Premium / luxury

Chapter 11 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Liters)

- 11.1 Key trends

- 11.2 Supermarkets and hypermarkets

- 11.3 Convenience stores

- 11.4 Specialty health food stores

- 11.5 Pharmacy and drug stores

- 11.6 Online retail

- 11.7 Foodservice sector

Chapter 12 Market Estimates and Forecast, By Sales Channel, 2021 - 2034 (USD Billion) (Kilo Liters)

- 12.1 Key trends

- 12.2 B2B

- 12.3 B2C

Chapter 13 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Liters)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Spain

- 13.3.5 Italy

- 13.3.6 Netherlands

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 Australia

- 13.4.5 South Korea

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.6 Middle East and Africa

- 13.6.1 Saudi Arabia

- 13.6.2 South Africa

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Yakult Honsha Co., Ltd.

- 14.2 Danone S.A.

- 14.3 Nestle S.A.

- 14.4 PepsiCo, Inc.

- 14.5 Coca-Cola Company

- 14.6 Lifeway Foods, Inc.

- 14.7 Harmless Harvest

- 14.8 KeVita (PepsiCo)

- 14.9 GoodBelly (NextFoods)

- 14.10 Chobani, LLC

- 14.11 Groupe Lactalis

- 14.12 Bio-K Plus International Inc.

- 14.13 Fonterra Co-operative Group Juicery

관련자료