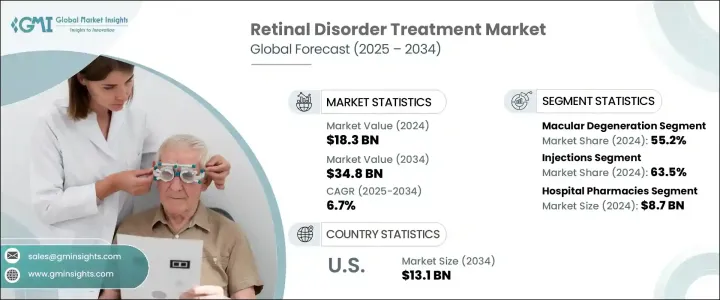

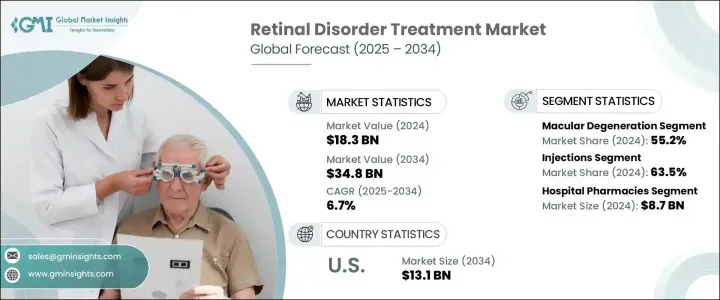

세계의 망막 질환 치료 시장은 2024년 183억 달러로 평가되었고, 당뇨병 망막증(DR)과 당뇨병 황반부종(DME) 등 합병증과 함께 당뇨병 유병률 증가에 견인되어 CAGR 6.7%로 성장할 전망이며, 2034년에는 348억 달러에 달할 전망입니다.

망막 질환 치료에는 항 VEGF 주사, 레이저 치료, 코르티코 스테로이드 치료, 유리체 수술과 같은 내과적, 외과적, 약학적 개입이 포함됩니다. 이러한 치료의 주된 목적은 망막 장애의 확대를 막고 시력을 유지 또는 회복하는 것입니다. 치료법의 선택은 증상의 중증도, 장애 단계, 환자의 눈 전체 건강 상태에 따라 달라집니다. DME는 특히 제2형 당뇨병 환자의 시력 저하의 주요 원인으로 시기적절한 개입과 전문적 치료의 필요성이 강조되고 있습니다.

서방형 안구 치료제와 같은 최근 치료법의 진보는 주사 빈도를 줄임으로써 환자의 컴플라이언스를 향상시키고 있습니다. 예를 들어, 어떤 종류의 주사기는 약물 전달을 지속하도록 설계되었으며, 잦은 안구 주사로부터 해방됩니다. 이러한 기술 혁신은 망막 질환의 보다 효과적인 해결책을 제공하는 동시에 치료 부담을 최소화하는 데 도움을 주고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 183억 달러 |

| 예측 금액 | 348억 달러 |

| CAGR | 6.7% |

2024년 시장은 황반변성, 특히 연령 황반변성(AMD)이 55%의 점유율을 차지했습니다. AMD는 주로 60세 이상에서 발병하며, 이 연령대에서 시력 저하의 주요 원인 중 하나입니다. 세계 인구의 고령화에 따라 고혈압이나 비만 등의 합병증이 AMD의 유병률을 더욱 악화시켜 지속적인 조사와 치료 혁신의 필요성을 촉구하고 있습니다.

주사 분야는 시장의 주요 견인 역할이며, 2024년에는 63.5%의 점유율을 차지했습니다. 유리체 내 주사는 AMD, 망막정맥폐쇄증, DME 등 망막 질환 치료에 일반적으로 사용되며, 항VEGF 요법은 신속한 치료 효과를 가져오기 때문에 이러한 질환 치료에 있어 유망한 결과를 나타내고 있습니다. Avastin, Eylea, Lucentis 등의 약제는 망막부종이나 신생혈관 감소에 효과적인 것으로 증명되었으며, 최종적으로는 환자의 시력을 개선하고 있습니다.

미국의 망막 질환 치료는 망막 질환에 걸리기 쉬운 인구의 고령화 및 고도의 유리체내 주사요법의 보급에 의해 미국 시장은 2024년의 71억 달러로 평가되었고, 2034년에는 131억 달러로 성장할 전망입니다. 게다가 유리한 상환 정책과 주요 제약업체의 강력한 위상이 계속해서 시장 확대에 박차를 가하고 있습니다.

세계의 망막 장애 치료 시장의 주요 기업은 Regeneron Pharmaceuticals, Bayer, AbbVie, Novartis, Pfizer, F. Hoffmann-La Roche 등이 있습니다. 이들 기업은 경쟁 정세에서 우위에 서기 위해 연구개발이나 신제품 개발에 투자하고 있습니다. 망막 장애 치료 시장에서 지위를 강화하기 위해, 각사는 제품 포트폴리오의 확충과 치료 기술의 진보에 주력하고 있습니다. 주요 발전 전략으로는 의약품 개발이나 유통에서 보완적인 전문 지식을 활용하기 위한 파트너십의 형성을 들 수 있습니다. 또한 기업은 혁신적인 약물 전달 시스템 및 상환 구조의 개선을 통해 환자 치료를 강화하고 있습니다.

The Global Retinal Disorder Treatment Market was valued at USD 18.3 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 34.8 billion by 2034, driven by the increasing prevalence of diabetes, along with its complications such as diabetic retinopathy (DR) and diabetic macular edema (DME). Retinal disorder treatments encompass a range of medical, surgical, and pharmaceutical interventions, including anti-VEGF injections, laser therapy, corticosteroid treatments, and vitrectomy. The primary goal of these treatments is to prevent further retinal damage and preserve or restore vision. The selection of a treatment depends on the severity of the condition, the stage of the disorder, and the overall health of the patient's eye. DME is a leading cause of vision loss, particularly among individuals with type 2 diabetes, highlighting the need for timely interventions and specialized care.

Recent advancements in treatment methods, such as sustained-release intraocular therapies, enhance patient compliance by reducing the frequency of injections. For example, certain injectable devices are designed for continuous drug delivery, offering relief from frequent eye injections. These innovations are helping to minimize the treatment burden while providing more effective solutions for retinal disorders.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.3 Billion |

| Forecast Value | $34.8 Billion |

| CAGR | 6.7% |

Macular degeneration, particularly age-related macular degeneration (AMD), dominated the market in 2024, accounting for a 55% share. AMD, which primarily affects individuals over 60 years old, is one of the leading causes of vision loss in this age group. As the global population ages, comorbidities such as hypertension and obesity further exacerbate the prevalence of AMD, driving the need for continued research and treatment innovation.

The injection segment is a key driver in the market, accounting for 63.5% share in 2024. Intravitreal injections are commonly used for treating retinal conditions like AMD, retinal vein occlusion, and DME. Anti-VEGF therapies have shown promising results in treating these conditions, as they offer rapid therapeutic responses. Drugs such as Avastin, Eylea, and Lucentis are proving effective in reducing retinal edema and neovascularization, ultimately improving visual acuity for patients.

United States Retinal Disorder Treatment Market is poised to grow from USD 7.1 billion in 2024 to USD 13.1 billion by 2034, driven by the aging population susceptible to retinal conditions and the widespread availability of advanced intravitreal injection therapies. Moreover, favorable reimbursement policies and the strong presence of key pharmaceutical manufacturers continue to fuel market expansion.

Key players in the Global Retinal Disorder Treatment Market include Regeneron Pharmaceuticals, Bayer, AbbVie, Novartis, Pfizer, and F. Hoffmann-La Roche. These companies are investing in R&D and new product development to stay ahead in the competitive landscape. To strengthen their position in the retinal disorder treatment market, companies are focusing on expanding their product portfolios and advancing treatment technologies. Key strategies include forming partnerships to leverage complementary expertise in drug development and distribution. Furthermore, companies are enhancing patient treatment through innovative drug delivery systems and improved reimbursement structures.